Hey everyone,

Welcome back to another bite to chew on.

You’ve probably heard that profit has taken over from high growth as the Northstar metric in DTC.

During the zero interest rate policy (ZIRP) era, money was cheap and plentiful.

It was easier to fund your business and then just…

…run it in the red - with the promise of future profitability somewhere down the road.

“Our CAC to LTV repayment timeline is only 24 months!”

Those days are over.

Free money is gone.

To survive you need to take more than you spend - as quickly as possible.

This is all true. But it’s only half the story.

Profitability is vital in e-commerce these days.

But so is cash flow.

And they are NOT the same thing. Correlated maybe. But not synonymous.

Today we’ll take you through the difference between the two -

And some of the things we do to manage both.

Understanding Profit

You need profit to survive. Full stop.

You can only sell $20 bills for $10 each for so long before you go out of business.

“No duh.”

We can feel you rolling your eyes on the other side of the screen.

But it’s a fundamental principle that many operators have to re-learn for various reasons.

As mentioned, one of those reasons was the era of -

Low interest rates,

Frothy venture investments, and

Big valuations for flashy growth numbers.

Back when a large capital raise seemed more important than notable margins.

But founders can just as easily be confused as seduced.

That’s because when you start out, profit seems simple.

Take what it costs to make your product. Quadruple it and you have your MSRP.

Voila.

Except things get complicated pretty quickly.

On top of your COGS, you have to consider shipping and freight.

Warehousing. Pick & pack costs.

Packaging and processing fees.

Discounts and marketing cost of acquisition (CAC).

These are the factors that go into understanding your contribution margin.

If you don’t account for every single expense that goes into delivering your product to the customer,

Then you can very quickly lose sight of how much you are actually making every time your phone goes “cha-ching”.

Because that noise could mean you just gave that customer a $20 bill - for $10.

Fighting for Profit

First things first.

You have to find a way to track your daily contribution margin per sales channel.

List out your COGS profile per SKU and then add the channel-related delivery costs on top.

For example, if you’re on Shopify, consider your payment processing and app fees. But if you’re also on Amazon, you’ll need to consider all of their related fees and costs. etc.

Next, make a habit of inspecting your channel CM, day in and day out.

This will force you to confront any factors that might push you into the red per purchase.

Of course, one of the big, rising costs these days is CAC.

Acquisition through marketing channels like Meta keeps getting pricier - increasing 222% on average since 2013.

So you need to fight for profit with every customer you land. Even at different points in the funnel.

If you understand your contribution margin,

Then you can also understand the impact of, say, increasing your AOV or your 90-day LTV

by just 10% will have on your bottom line.

Which is why -

Bundling

Upsells

Cross-sells

Subscriptions

Network offers

Have become such important tactics in DTC.

Driving incremental revenue from every new customer helps you to amortize that initial cost of acquiring them.

Which will help push your CM into the black.

Tool of the Week

Speaking of profit…

Have you ever heard of a tool that:

Requires little to no setup from your end

Delivers immediate impact to your bottom line

Only makes money when you make money

Sounds like a dream, right?

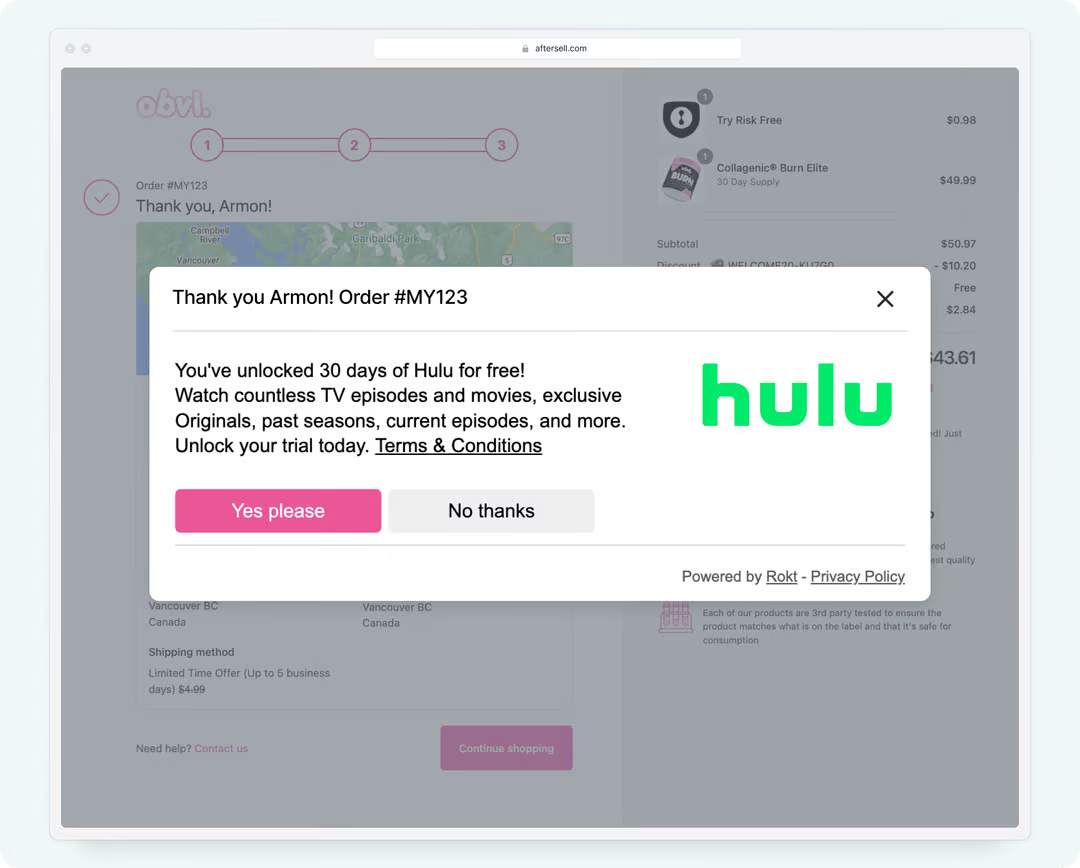

Think again…check out Network Offers from Aftersell.

Here’s how it works

A blue-chip company like HULU or Amazon Prime wants to reach the same customer as you.

The blue-chip company will place an ad on your checkout or thank-you page where they serve up a relevant offer.

If the customer takes the offer - let’s say 2-months free HULU subscription - you get paid

Yup. it’s easy.

We’ve seen them do this for us with no effort on our side. And no extra fees.

“But I don’t want to spam my users with random offers.”

Don’t worry, they thought of that.

Aftersell makes sure it’s not just random offers – their machine learning tech only suggests offers they judge to be relevant for that person.

(See example below)—>

The results?

We’ve added $0.45 in PURE profit per transaction (essentially covering our shipping and fulfillment costs).

So if you want to join other top brands like Jones Road Beauty and Hexclad in effortlessly boosting your AOV, check out Aftersell’s Network offers.

Based on our experience, we can’t recommend them enough.

Understanding cash flow

Alright, let’s get into the cash side of things...

Even if you’re technically keeping more than you’re spending.

It doesn’t mean you’re in the clear.

You can make a profit on every transaction and still struggle with cash flow.

Why?

Well…your business will sometimes face major expenditures. Big bills like taxes or inventory purchase orders can come in waves.

And fixed expenses like

Rent ❌

Salary ❌

Benefits ❌

Supplies ❌

- All the other stuff that keeps the lights on - it’s always there.

No matter how sales are going. High, low. Big, small.

Those bills greet you every month.

(Those of you who run a seasonal business are acutely aware of this pain.)

So the combination of:

➕ A big purchase

➕ Dipping gross revenue

➕ And fixed expenses

Can 🟰 cash flow problems. Even if every one of your sales is profitable.

Meaning - being positive “net per SKU” is great, but you also have to hit a certain revenue amount to pay your bills every month.

You can;t just optimize purely for efficiency on each sale.

You also need a certain volume of sales to make money. Profitable at scale so you can pay your bills.

Managing for cash flow

Here’s where you need to get comfortable with spreadsheets and transparency.

At Obvi, we use a few to manage our cash:

We create a 13-to-26-week cash flow analysis so we have visibility into our “cash window”. Here’s a quick primer on how.

We send a daily P&L to our execs and board members. Here’s how we leverage this information.

We forecast our financials and inventory. For more information on all of these tactics, check out our Obvi Finance School resource here.

With these processes in place, you will get a picture of your cash and a sense of how it flows in and out of your business.

Also - this will help you get ruthless about your costs.

Review your subscriptions, tools, and platform fees regularly.

Determine if you really need everything in your tech stack. Look for better value where you can.

Negotiate with everyone else.

When a negative is a positive

That brings us to the cash conversion cycle.

That’s just another name for how long it takes to turn the money you spend on inventory back into cash through sales.

And despite the name, a negative cash conversion cycle is the best thing to have.

Because it means you are selling your inventory before you have to pay for it.

A negative cash conversion cycle can be rocket fuel because your major cost (inventory) is being paid out of the revenue you’re making off of it.

In fact, it can make sense to trade a few points of margin in return for more favorable payment terms.

(Remember when we said cash flow and profit are not the same thing?)

Some key ways to improve your cash conversion cycle:

As mentioned, negotiate with vendors and suppliers for longer payment terms. Even if you pay a little bit more for your product

Look for tools and offers that can extend your runway, such as credit cards with 60-day no-payment terms

Accelerate your inventory-to-sales pace with just-in-time inventory if possible

Consider outside financing

Of course, funding your business often comes down to outside financing, to one degree or another.

Managing your cash well can mean avoiding heavy or ruinous debt.

But some bills are just too big to pay out of pocket.

Equity is very expensive money (and not really an option for many).

Which leaves traditional lenders and FinTechs.

If you have an established biz with good margins and projectable growth, you can work with a bank on a loan or line of credit.

But remember - banks like to loan money to those who don’t really need it.

So be sure to plan ahead and apply for bank financing before the cash crunch happens.

The other option - Fintechs or Neo Banks - usually offer revenue-based financing.

This is usually much less painful to apply for and easier to acquire.

But you need to understand the payment terms that come with these offers.

They can involve higher APR’s and will take a percentage of your daily revenue until the loan is repaid.

Revenue financing can be great in a pinch. Just be sure to look before you leap.

Sum it up

Profit is necessary but not sufficient to run a successful DTC business these days.

You need to understand your COGS profile and how much contribution margin you;e netting - preferably on a daily basis across your sales channels.

But you also need to manage your cash.

It only takes:

one big PO,

one large tax bill,

one down month, or

one overly ambitious inventory forecast

To get you in trouble.

Be fastidious about forecasting your business, as well as negotiating your payment terms and minding your costs.

At Obvi, we have tackled all of these challenges. And continue to refine our processes each and every day.

It’s not easy, but if we can do it -

So can you.

All the best,

Ron & Ash